Audit General’s Report and Audit YE 31st March 2025

Auditor General’s report and audit opinion

I certify that I have completed the audit of the Annual Return for the year ended 31 March 2025 of Broughton Community Council. My audit has been conducted on behalf of the Auditor General for Wales and in accordance with the requirements of the Public Audit (Wales) Act 2004 (the 2004 Act) and guidance issued by the Auditor General for Wales.

Audit opinion: Qualified

Except for the matters reported below in my Basis for Qualification, on the basis of my audit, in my opinion no matters have come to my attention to give cause for concern that, in any material respect, the information reported in this Annual Return:

- has not been prepared in accordance with proper practices;

- that relevant legislative and regulatory requirements have not been met;

- is not consistent with the Council’s governance arrangements; and

- that the Council does not have proper arrangements in place to secure economy, efficiency and effectiveness in its use of resources.

Basis of Qualification

Accounting Statement

I am unable to conclude whether or not the Accounting Statement fairly present the Council’s income and expenditure and financial position:

• The Council did not provide invoices for 3 material transactions. Therefore, I am unable to conclude whether or not the Accounting Statement fairly presents the Council’s income and expenditure.

Annual Governance Statement

In my opinion, the Annual Governance Statement is not consistent with the Council’s internal controls and governance arrangements for the year:

- Section 50 of the Democracy and Boundary Commission Cymru etc. Act 2013 requires the Council to publish its audited accounts online. Regulation 5 of the Accounts and Audit (Wales) Regulations 2014 requires the Council to publish the Annual Governance Statement alongside the accounts. Regulation 15 of the 2014 Regulations requires the Council to publish along with the accounts, any certificate, opinion, or report issued, given or made by the Auditor General. The Council has failed to publish its qualified audit reports from previous years.

- The Local Government and Elections (Wales) Act 2021 requires the Council to create and publish a plan for councillor and staff training. The Welsh Government provides statutory guidance on this, which states that the plan must be approved by the full council and include details on the type of training,

Page 1 of 3 – Auditor General’s report and audit opinion – please contact us in Welsh cysylltwch â ni’n Gymraeg neu’n Saesneg.

participant numbers, timeframe, and cost. The Council has not met its obligation under the Local Government and Elections (Wales) Act 2021 to create and publish a training plan for members.

- The Council does not publish a register of members’ interests as required by section 81 of the Local Government Act 2000.

Other matters and recommendations

I draw the Council’s attention to the following matters and recommendations which do not affect my audit opinion but should be addressed by the Council.

Chair’s Allowance

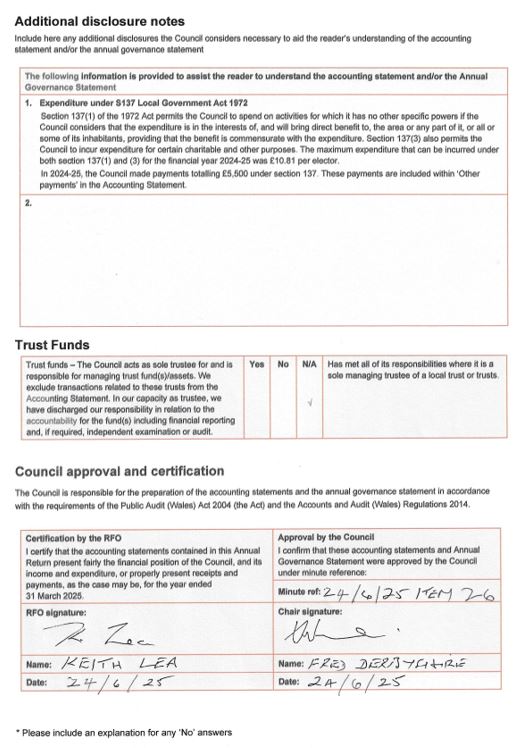

The Chair was paid £300 in 2024/25 and this allowed under the Independent Remuneration Panel for Wales’ guidelines. However, we were unable to identify whether this payment was taxed.

We recommend that the Council reviews the Independent Remuneration Panel for Wales’ guidelines and ensures that the appropriate level of taxation is levied.

Reserves Balance

The Local Government Finance Act 1992 only allows the Council to set a precept to fund planned expenditure and requires it to take its reserves into account when setting the precept. It is not clear from the information provided for audit whether or not the Council has taken its significant reserves balance into account when setting the precept.

To ensure that it sets a lawful precept, we recommend that the Council reviews its reserves and its plans to apply these reserves when setting its future budgets and precept. Further guidance is found in the Practitioners’ Guide.

Developing a Vision for the Community

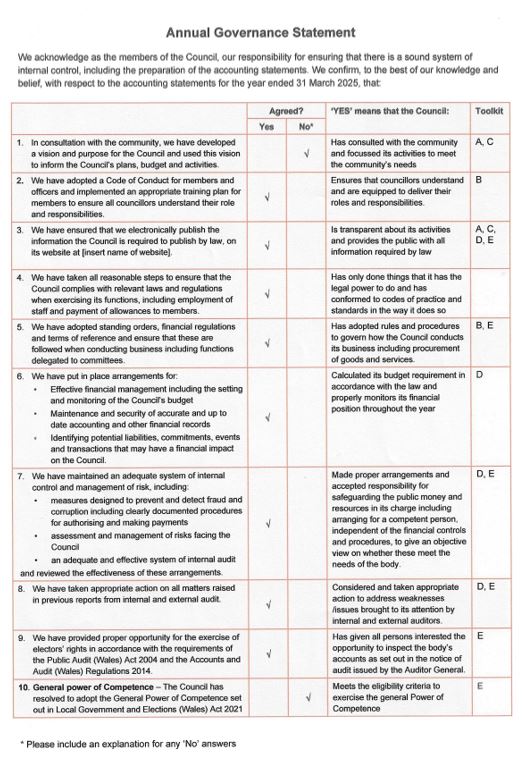

I draw attention to the negative response to assertion 1 in the Annual Governance Statement. In exercising its statutory functions, the Council will benefit from having a clear vision for its community that has been developed in partnership / consultation with all sections of the community. Developing this vision will help inform Council plans, budgets and activities to ensure the Council best works with and in the interests of the community.

Further information is provided in the Finance and Governance Toolkit for Community and Town Councils.

Page 2 of 3 – Auditor General’s report and audit opinion – Please contact us in Welsh Cysylltwch â ni’n Gymraeg neu’n Saesneg.

Information provided for audit

The Council did not provide the arrangements for making payments document or the contract of employment for an additional Council staff member as requested in our annual audit notice.

We recommend that the Council reviews the prospective annual audit notice and provides all of the documents that are requested for audit.

Immaterial Misstatement in the Accounting Statement

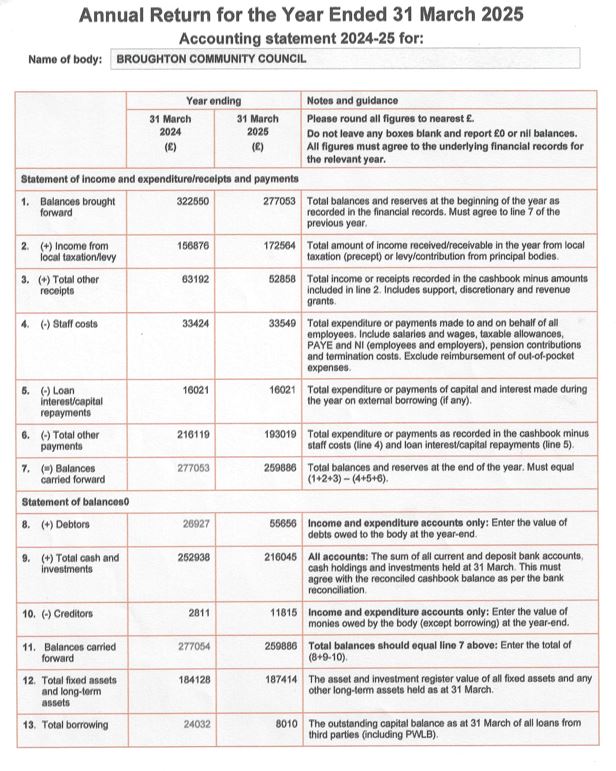

Line 8 of the Accounting Statement for the year ended 31st March 2025 contains a non-material variance to the Council’s cashbook. The balance is line 8 is reported as £55,656. However, the Council’s cashbook reports a balance of £53,979.

We recommend that the Council checks the accuracy of the accounting statement and makes the necessary corrections before the accounts are approved.

There are no further matters I wish to draw to the Council’s attention.

| Date: 18/02/2026 |

Page 3 of 3 – Auditor General’s report and audit opinion – Please contact us in Welsh Cysylltwch â ni’n Gymraeg neu’n Saesneg.